Saving money is an important aspect of personal finance. It allows you to have a safety net in case of emergencies or unexpected expenses. There are different kinds of accounts that can be used to save money, so what is the best account to save money in? In this blog post, we will describe four types of accounts, including interest-earning checking accounts, savings accounts, certificates of deposit, and money market accounts.

Interest‐earning Checking Accounts

What Is It?

An interest-earning checking account is a type of checking account that pays interest on the balance in the account. The interest rate on these accounts is usually low, but it is still a good option if you want to earn some interest while keeping your money easily accessible. These accounts also offer the convenience of a traditional checking account, such as the ability to write checks and make withdrawals using a debit card.

Pros

Interest-earning checking accounts are easy to use and offer quick access to your funds.

They offer a higher interest rate than a regular checking account.

You can usually link your interest-earning checking account to other accounts to transfer funds easily.

Cons

The interest rate is usually lower than other savings accounts.

You may be required to maintain a minimum balance to avoid fees.

A savings account is a type of account designed for long-term savings. It typically offers a higher interest rate than a checking account, but it may have some restrictions on withdrawals. You can open a savings account at a bank or credit union, and you can deposit or withdraw money at any time. This is the best account to save money in if you are fine with limited withdrawals.

Pros

Savings accounts are easy to open and use.

They offer a higher interest rate than a checking account.

Some savings accounts offer tiered interest rates based on your balance.

Cons

Savings accounts may have minimum balance requirements to avoid fees.

You may be limited to a certain number of withdrawals per month.

Certificates of Deposit

What Is It?

A certificate of deposit is like a savings account, but it is not as liquid as a savings or checking account. CD’s have a fixed period of existence, which can be six months, a year, or five years. While the bank holds your money in this account, it accrues interest. Then at the maturity date, you will get back the money you put into it as well as the interest the account accrued. CD’s also have early withdrawal penalties, meaning you cannot withdraw the money before the maturity date.

Pros

CDs offer a higher interest rate than a savings account.

You can choose the length of time that works best for you.

CDs are a safe investment option.

Cons

You cannot withdraw the money until the CD reaches maturity.

If you withdraw the money early, you will incur a penalty.

Money market accounts offer a higher interest rate than a regular checking account.

They offer the convenience of a checking account with the interest-earning power of a savings account.

Cons

Money market accounts may have higher minimum balance requirements than other accounts.

They may have fees if your balance falls below the minimum requirement.

In conclusion

There are different kinds of accounts that can be used to save money. The best account for you will depend on your financial goals and needs. Interest-earning checking accounts, savings accounts, certificates of deposit, and money market accounts are all great options to consider. Some accounts allow for more regular deposits and withdrawals while other accounts require a single deposit to stay in the account for for a specified amount of time. Make sure to do your research and choose the best account to save money in (that fits your needs).

When it comes to finances, there are many metrics that people use to assess their financial health. One of the most important metrics is net worth. Net worth is the value of everything you own minus the value of everything you owe. It is a way to measure your overall financial position and is a useful tool for assessing your progress towards your financial goals.

Your net worth is a snapshot of your financial situation at a specific point in time. It can fluctuate over time as you accumulate or reduce assets and debts. Your net worth is important because it can help you make informed financial decisions, such as whether to take on additional debt or invest in assets.

How to Create a Net Worth Statement

Creating a net worth statement is a simple process that involves adding up the value of everything you own and subtracting the value of everything you owe. Here are the steps to create a net worth statement:

Step 1: List Your Assets

Start by creating a list of all the assets you own. This includes your cash savings, investments, retirement accounts, real estate, vehicles, and any other assets that have value. Be sure to include the current market value of each asset. The original value of the asset will not accurately reflect the increase in value due to inflation.

Once you have a list of all your liabilities, add up their total value. This will give you the total amount of debt you owe.

Step 5: Subtract Your Liabilities from Your Assets

Finally, subtract the total value of your liabilities from the total value of your assets. The result is your net worth.

Here is an example to illustrate this process:

Assets:

Cash savings: $10,000

Investments: $50,000

Retirement accounts: $100,000

Real estate: $250,000

Vehicles: $30,000 Total assets: $440,000

Liabilities:

Credit card debt: $5,000

Student loans: $20,000

Mortgage: $200,000 Total liabilities: $225,000

Net worth: $215,000 ($440,000 – $225,000)

Tips for Improving Your Net Worth

If you want to improve your net worth, there are several strategies you can use. Here are a few tips to help you get started:

Increase Your Income

One of the easiest ways to to do this is to increase your income. This can be done by taking on a side job or by asking for a raise at your current job. You can also participate in some kind of professional development such as getting a certificate or a degree. Consequently, this may help you get a raise at your current job or may help you get a raise by switching jobs.

Photo by John Guccione www.advergroup.com on Pexels.com

Reduce Your Expenses

Another way to improve it is to reduce your expenses. This can be done by cutting back on unnecessary expenses or by finding ways to save money on essential expenses.

Pay Down Your Debt

Paying down your debt is another effective way to improve. This can be done by making extra payments on your loans or by consolidating your debt into a single, lower-interest loan. For example, you can switch your payment schedule of your car loan from monthly to bi-weekly and get in one extra payment a year!

Invest Wisely

Investing in assets that appreciate in value is an effective way to grow your net worth over time. However, it’s important to remember that investing always carries some level of risk. While stocks, real estate, and other investments may have a track record of increasing in value over time, they can also experience downturns and losses. It’s important to conduct thorough research and seek professional advice before investing in any asset.

One of the benefits of investing in stocks is that they offer the potential for high returns. Stocks represent ownership in a company and their value can increase as the company grows and becomes more profitable. However, stocks also carry the risk of market volatility and can experience sharp declines in value. It’s important to diversify your stock portfolio and invest in a range of companies to minimize risk. Investing in a fund, such as a mutual fund or index fund, can help you diversify because they include many different stocks.

Finally, it’s important to avoid taking on more debt than you can afford. This can be done by creating a budget and sticking to it, or by avoiding high interest loans and credit cards. By keeping your debt levels under control, you can avoid paying excessive interest charges and fees, and instead focus on building your net worth over time. Remember, a positive net worth is a key indicator of financial health and stability, so it’s worth taking the time to create a net worth statement and work towards improving it. With discipline and good financial habits, anyone can achieve a strong net worth and enjoy the benefits of financial freedom and security.

Setting goals is a critical step in achieving success in any aspect of life. Whether it’s personal or professional, goals give you direction, motivation, and a sense of purpose. However, setting goals is not enough; you need to set them effectively to achieve them. In this blog post, we will discuss how to set goals and how SMART goals can help you achieve them.

How to Set Goals:

Identify your purpose: The first step in setting goals is to identify your purpose or what you want to achieve. Ask yourself what you want to accomplish and why it’s important to you. Having a clear purpose will help you stay motivated and focused.

Make your goals specific: Once you’ve identified your purpose, make your goals specific. Vague goals like “get in shape” or “make more money” won’t help you achieve much. Instead, make your goals specific, measurable, and achievable.

Break it down: It’s essential to break down your goals into smaller, manageable steps. This will help you track your progress, stay motivated, and avoid feeling overwhelmed. Make a list of the actions you need to take to achieve your goals.

Set a timeline: Set a timeline for achieving your goals. This will help you stay focused and motivated. A deadline will also help you track your progress and adjust your actions if necessary.

Track your progress: Keep track of your progress regularly. This will help you see how far you’ve come and what you need to do to achieve your goals.

SMART is an acronym for Specific, Measurable, Achievable, Relevant, and Time-bound. This is a fantastic method for setting goals effectively. Here’s what each letter of the acronym means:

Specific: Your goals should be clear and specific. Avoid vague goals like “get in shape” or “make more money.” Instead, make your goals specific, like “lose 10 pounds” or “increase my income by $500 a month.”

Measurable: Your goals should be measurable. You should be able to track your progress and measure your success. For example, if your goal is to save money, measure your progress by adding up how much you put into your savings account.

Achievable: Your goals should be achievable. Don’t set goals that are impossible to achieve. Instead, set goals that challenge you but are still achievable. An impossible goal would be buying a million dollar house when you make $80,000 per year. An achievable goal would be to put 5% of your yearly income into a retirement account.

Relevant: Your goals should be relevant to your purpose. Ask yourself how achieving your goals will help you achieve your purpose. If you want to be a therapist, going to school for accounting would not be relevant and would not help you achieve that purpose.

Time-bound: Your goals should have a deadline. A deadline will help you stay focused and motivated. It will also help you track your progress and adjust your actions if necessary.

All in all, setting goals is essential for achieving success in any aspect of life. To set goals effectively, identify your purpose, make your goals specific, break them down, set a timeline, and track your progress. Remember, setting goals is just the first step. You need to take action and stay committed to achieving them.

However, setting goals and following the SMART framework is just the beginning. Achieving those goals requires a lot of effort, dedication, and hard work. Here are some additional tips that can help you achieve your goals:

Stay Motivated: Motivation is key to achieving your goals. Find ways to keep yourself motivated and remind yourself why you set those goals in the first place. You can use positive affirmations, visualize yourself achieving your goals, or reward yourself for making progress.

Be Flexible: Life can be unpredictable, and things don’t always go according to plan. Be open to adjusting your goals if necessary. It’s okay to make changes to your goals if they no longer serve your purpose or if circumstances change.

Find Support: Achieving your goals can be challenging, but it’s easier when you have support. Surround yourself with people who believe in you and support your goals. You can also find a mentor, join a support group, or see a financial counselor.

Celebrate Your Successes: Celebrate your successes, no matter how small they are. Celebrating your successes can help you stay motivated and remind you of how far you’ve come.

Learn from Your Failures: Failure is a part of the journey. Don’t let failures discourage you. Instead, use them as an opportunity to learn and grow. Analyze what went wrong and use that knowledge to make better decisions in the future.

Setting goals and following the SMART framework is an important step in achieving success. However, it’s just the beginning. Achieving your goals requires hard work, dedication, and a willingness to learn and grow. By following these additional tips, you can increase your chances of achieving your goals and living the life you want. Good luck on your journey!

Struggling to stick to your financial goals? My Financial Goals Workbook can help—learn more here.

Your credit report is a crucial tool that lenders, banks, and credit card companies use to evaluate your financial history and determine your creditworthiness. So, what information is on a credit report? It contains a wealth of information about your financial habits, including your credit accounts, payment history, and outstanding debts. In this blog post, we will discuss the information that is typically included in a person’s credit report.

Personal Information

Name

Date of Birth

Social Security Number

Current and Previous Addresses

Employment History

Your personal information is very important because it helps credit bureaus accurately identify and track your credit history. It is important to review this information regularly to make sure that it is up to date and correct. Any errors in your personal information can lead to problems down the road, such as difficulty getting approved for credit or loans. In addition to the basic personal information, some credit reports may also include additional data, such as your phone number or email address. However, it is important to note that your credit report does not include sensitive information such as your religion, ethnicity, medical history, criminal record, or political affiliation. This is because the Fair Credit Reporting Act (FCRA) prohibits credit bureaus from including this type of information in credit reports.

The credit accounts section of your credit report is one of the most important sections, as it provides a detailed history of your credit activity. This section can also help potential lenders determine whether you are a responsible borrower who pays bills on time. In addition to the payment history, this section will also show whether the account is current or delinquent. If an account is delinquent, the credit report will show how many payments were missed and how many days past due the account is.

The credit accounts section of your credit report can also provide insight into your credit utilization rate, which is the amount of credit you are currently using compared to your total available credit limit. A high credit utilization rate can negatively impact your credit score, because it suggests that you may be relying too heavily on credit and may have difficulty paying your bills on time.

It is important to note that not all credit accounts are reported to credit bureaus. Some creditors may not report to all three major credit bureaus, or they may not report at all. This can result in incomplete or inconsistent information on your credit report. It is also important to review this section of your credit report regularly to ensure that all the information is accurate and up-to-date. If you find any errors or inaccuracies, you should contact the creditor and credit bureau immediately to have the information corrected.

Public Accounts

Bankruptcies

Tax Liens

Judgments

The public records section of your credit report can have a significant impact on your creditworthiness. Consequently, if you have a bankruptcy or tax lien on your credit report, it can be difficult to obtain new credit or loans, and may result in higher interest rates or fees. Credit reports do not automatically include all public records. Credit bureaus may obtain this information from public records databases, but they may not have access to all public records information.

If you have a bankruptcy or tax lien on your credit report, it is important to take steps to repair your credit. This may involve working with a credit counselor or financial counselor to develop a plan to pay off your debts and improve your credit score. You may also want to consider obtaining a secured credit card or other type of credit account to help rebuild your credit.

It is important to note that some public records, such as civil suits or arrests, are not included in your credit report. The Fair Credit Reporting Act (FCRA) prohibits credit bureaus from including certain types of information in credit reports, including civil suits or arrests, unless the information is related to a financial transaction.

Inquiries

Hard Inquiries

Soft Inquiries

The inquiry section of your credit report reveals the frequency and recency of credit applications, with hard inquiries impacting your credit score for up to 12 months, while remaining visible for two years. Multiple hard inquiries can decrease your credit score by a few points each, with a greater impact when clustered together.

Conversely, soft inquiries, including personal credit checks and pre-approved credit offers, have no impact on your credit score and are not visible to lenders. Furthermore, credit scoring models consider multiple inquiries within a short timeframe for a specific loan or credit product as a single inquiry, acknowledging consumers’ tendency to rate-shop.

To minimize hard inquiries, only apply for credit when needed, and avoid multiple applications within a short period. Using credit monitoring services can also help keep track of your credit report and alert you to changes or new inquiries.

Your credit score is an important factor that lenders and creditors use to determine your creditworthiness. Due to this, a good credit score can help you qualify for better interest rates, higher credit limits, and more favorable terms on loans and credit accounts. Your credit score is calculated based on the information in your credit report, which includes your payment history, credit utilization, length of credit history, types of credit accounts, and recent credit inquiries.

FICO scores are the most widely used credit scoring model and are used by most lenders and creditors. FICO scores range from 300 to 850, with a score of 670 or higher generally considered to be a good credit score. VantageScores are another type of credit score that is becoming increasingly popular. The VantageScore range is from 300 to 850, and a score of 661 or higher is generally considered to be a good credit score. While FICO scores and VantageScores are calculated using a similar algorithm, they may take into account different factors and weight them differently.

Credit Scores Can Vary

It is important to note that your credit score can vary depending on which credit reporting agency is used to calculate it. Each credit reporting agency may have slightly different information on your credit report, which can impact your credit score. However, regardless of the credit reporting agency, it is important to maintain a good credit score by making payments on time, keeping your credit utilization low, and avoiding unnecessary credit applications. Additionally, regularly checking your credit report and using credit monitoring services can help you stay on top of your credit and quickly address any issues that may arise.

Credit scores are not a one-time calculation and can change over time, depending on your credit behavior. For this reason, regularly reviewing your credit report and credit score can help you identify areas for improvement and take steps to build and maintain good credit.

In addition to working with a credit counselor or financial advisor, you may also want to consider using credit monitoring services or credit score simulators to help you stay on top of your credit. These tools can provide you with alerts and insights about your credit report and score, as well as tips and recommendations for improving your creditworthiness.

Places You Can Check Your Credit Report

AnnualCreditReport.com – This website allows you to request a free credit report from each of the three major credit reporting agencies (Equifax, Experian, and TransUnion) once per year.

Credit Karma – This website offers free credit monitoring and access to your credit report and credit score.

In Conclusion

Additionally, your credit report is a crucial tool that lenders and creditors use to evaluate your creditworthiness. It contains a wealth of information about your financial habits, including your credit accounts, payment history, and outstanding debts. By understanding the information that is included in your credit report, you can take steps to improve your credit score and increase your chances of being approved for credit. Be sure to check your credit report regularly and dispute any errors that you find.

Managing personal finances can be a daunting task, particularly in the current economic climate. With so many financial products and services available, it can be challenging to know where to begin, let alone how to make informed decisions about money management. This is where financial planners and financial counselors come in, providing advice and guidance to help individuals and families navigate the complexities of personal finance. Continue reading to learn more about choosing which professional will work better for you: an accredited financial counselor vs certified financial planner.

Accredited Financial Counselor vs. Certified Financial Planner

Financial planners and financial counselors are two types of professionals who offer financial guidance, but they approach their work in different ways.

Financial planners focus on helping clients develop and implement long-term financial plans to achieve their goals, such as saving for retirement or a child’s education. They often have a background in finance or accounting and may hold certifications like Certified Financial Planner (CFP) from the Certified Financial Planner Board of Standards.

Financial counselors, on the other hand, concentrate on helping clients address immediate financial concerns, such as managing debt or creating a budget. They may also assist with long-term planning, but their primary focus is on helping clients improve their current financial situation. Financial counselors typically have a background in counseling, social work, or a related field and may hold certifications like Accredited Financial Counselor (AFC) from the Association for Financial Counseling and Planning Education.

The Certified Financial Planner Board of Standards (CFP Board) is a professional organization that sets ethical and professional standards for financial planners. The financial planning industry widely recognizes the CFP certification as a symbol of excellence and the CFP Board offers it to professionals.

To earn the CFP certification, candidates must complete a rigorous education program that covers topics like financial planning, taxes, and retirement planning. They must also pass a comprehensive exam and meet experience and ethical requirements.

The education program for the CFP certification requires a bachelor’s degree or higher, with the majority of the coursework focused on financial planning. The exam is comprehensive and tests candidates on their knowledge of financial planning, taxes, investments, insurance, and retirement planning. The experience requirement for the CFP certification is at least three years (6,000 hours) of full-time work experience in the financial planning industry. Additionally, CFP candidates must adhere to a strict code of ethics and complete continuing education courses to maintain their certification.

Accredited Financial Counselor

The Association for Financial Counseling and Planning Education (AFCPE) is a professional organization that sets ethical and professional standards for financial counselors. The organization offers the Accredited Financial Counselor (AFC) certification, which is recognized as a symbol of excellence in the financial counseling industry.

To earn the AFC certification, candidates must complete a comprehensive education program that covers topics like budgeting, credit management, and financial counseling. They must also pass a comprehensive exam and meet experience and ethical requirements.

The education program for the AFC certification does not require a bachelor’s degree. However, candidates must have a high school diploma or equivalent and complete 1000 hours of financial counseling experience. The exam for the AFC certification is comprehensive and tests candidates on their knowledge of financial counseling, budgeting, debt management, and credit counseling. AFC candidates must also adhere to a strict code of ethics and complete continuing education courses to maintain their certification.

While both the CFP and AFC certifications demonstrate a high level of expertise in the financial industry, there are some key differences between the two.

The CFP certification focuses primarily on financial planning, while the AFC certification focuses on financial counseling. As a result, financial planners with the CFP certification are more likely to help clients with long-term planning and investment management, while financial counselors with the AFC certification are more likely to focus on budgeting and debt management.

Another difference between the two certifications is the education requirements. To earn the CFP certification, candidates must complete a bachelor’s degree or higher, while the AFC certification only requires a high school diploma or equivalent. However, both certifications require candidates to complete a comprehensive education program and pass a rigorous exam.

Additionally, the experience requirements for each certification differ. CFP candidates must have at least three years (6,000 hours) of full-time work experience in the financial planning industry, while AFC candidates must have 1000 hours of financial counseling experience. This difference reflects the focus of each certification, with CFPs more likely to work with clients on long-term planning and investments, while AFCs are more likely to work with clients on day-to-day budgeting and debt management.

Choosing Between a CFP and an AFC

Deciding whether to work with an accredited financial counselor vs certified financial planner depends on your individual needs and financial goals. If you are focused on long-term planning, such as retirement or saving for a child’s education, a financial planner may be the best choice. On the other hand, if you are struggling with day-to-day budgeting or managing debt, a financial counselor may be the better fit.

It is also important to consider the qualifications of the financial professional you choose to work with. Both the CFP and AFC certifications are recognized as symbols of excellence in their respective fields, but they have different focuses and requirements. Therefore, it is important to choose a financial professional who has the appropriate qualifications and experience for your specific needs.

In conclusion, both financial planners and financial counselors play important roles in helping individuals and families manage their personal finances. While they have different focuses and certifications, both are highly trained professionals who can provide valuable guidance and support to those seeking to improve their financial situation. By understanding the differences between these two types of professionals and their respective certifications, you can make an informed decision about who to work with and how to achieve your financial goals.

Managing finances can be a daunting task for many people, especially when unexpected expenses or changes in income occur. A financial counselor can offer guidance and support to individuals and families to help them manage their finances effectively. They help clients create a budget, reduce debt, save for the future, and make informed financial decisions.

The Association for Financial Counseling and Planning Education (AFCPE) is a non-profit organization that is committed to improving the financial well-being of individuals and families. The organization was established in 1984 and has since become a leading provider of financial counseling and education in the United States.

The AFCPE provides financial counseling and education training to financial counselors and planners, as well as research and certification. The AFC certification is a professional certification for individuals who provide financial counseling services. The certification is a rigorous process that requires a combination of education, experience, and an exam.

What is the Certification Process?

The AFC certification process consists of three main steps: education, experience, and an exam. Additionally, they are required have at least 1,000 hours of experience in financial counseling within the past five years. They can complete these hours through paid or volunteer work. Once they have completed these requirements, they are eligible to take the AFC exam, which covers financial counseling principles, practice, and ethics.

The AFC certification is a significant achievement for financial counselors, and it demonstrates their commitment to providing quality financial counseling services to their clients. The certification is valid for two years, after which the financial counselor must complete 30 hours of continuing education to maintain their certification.

What Can A Financial Counselor Do?

Financial counselors with the AFC certification can offer a range of services to their clients, including budgeting, debt management, credit counseling, retirement planning, and more. They work with individuals, couples, and families in order to help them achieve their financial goals and improve their financial well-being.

Financial counselors play a crucial role in helping people manage their finances, especially in times of financial hardship or uncertainty. They can provide valuable guidance and support to help clients overcome financial challenges and achieve their financial goals. The AFCPE and the AFC certification provide financial counselors with the necessary training and certification to become competent and reliable professionals in the field of financial counseling.

Financial counseling is an essential service that helps individuals and families manage their finances effectively. The AFCPE and the AFC certification play a critical role in providing financial counselors with the necessary training, certification, and support to help their clients achieve their financial goals. The AFC certification process is rigorous but rewarding. Consequently, it demonstrates the financial counselor’s commitment to providing quality services to their clients. Financial counselors with the AFC certification offer a range of services that can help clients improve their financial well-being and achieve financial stability. You can go to Find An AFC and enter your location to see if a financial counselor is near you!

Personal finance is a topic that affects everyone, regardless of age, income, or background. At its core, personal finance is about managing our money in a way that aligns with our goals and values. While there are many different strategies and approaches to managing our finances, one important factor to consider is our locus of control. Our locus of control is our beliefs about whether we have control over the outcomes in our lives. In this blog post, we’ll explore the concept of locus of control and how it relates to personal finance. You can also learn about the link between Maslow’s Hierarchy of Needs and personal finance in this article.

Internal Locus of Control

Locus of control refers to the degree to which people believe they have control over the events in their lives. People with an internal locus of control believe that their actions and decisions have a direct impact on the outcomes they experience. In contrast, people with an external locus of control believe that their outcomes are largely determined by external factors such as luck, fate, or the actions of others.

In the context of personal finance, our locus of control can have a significant impact on our financial well-being. For example, people with an internal locus of control may be more likely to take an active role in managing their finances, such as creating a budget, tracking their spending, and investing for the future. They may also be more likely to take responsibility for their financial mistakes and seek out ways to improve their financial situation.

On the other hand, people with an external locus of control may be more likely to feel helpless or resigned in the face of financial challenges. They may view their financial situation as something that is largely out of their control and may be less likely to take action to improve it. For example, someone with an external locus of control may feel that they are simply “bad with money” and that there is little they can do to change that.

Of course, it’s worth noting that our locus of control is not fixed – it can change depending on the situation or the stage of life we are in. For example, someone who has always had an internal locus of control may begin to feel more helpless in the face of financial challenges if they experience a significant setback such as a job loss or a major illness. Similarly, someone with an external locus of control may develop a greater sense of agency and control over their finances through education and practice.

So, how can we cultivate an internal locus of control when it comes to personal finance? Here are a few strategies to consider:

Educate yourself. One of the best ways to feel more in control of your finances is to learn as much as you can about personal finance. This can include reading books and articles, attending financial workshops, or working with a financial advisor. By increasing your knowledge and understanding of financial concepts, you can feel more confident in your ability to make informed decisions about your money.

Set goals. When you have clear financial goals, it can be easier to take action and make progress. Consider setting short-term and long-term goals for your finances, such as paying off debt, building an emergency fund, or saving for retirement. Write these goals down and create a plan for achieving them. This can help you feel more in control of your finances and motivated to take action.

Take action. It’s one thing to have financial goals, but it’s another thing entirely to take action to achieve them. Consider creating a budget, tracking your spending, automating your savings, and seeking out ways to increase your income. The more action you take, the more in control you will feel.

Reflect on your mindset. Finally, it’s worth taking time to reflect on your mindset and beliefs about money. Do you view money as something that is scarce and hard to come by, or as something that can be earned and managed with intention? Do you tend to blame external factors for your financial challenges, or do you take responsibility

Some Things Are Actually Out Of Your Control

While having an internal locus of control can make a tremendously positive impact on your life and finances, it is important to remember that there are things that are outside of your control. If you do find yourself in a situation that is outside of your control, there are almost always resources available both locally and nationally to help you find your way. Remember that even in those situations, you do still have some control and can affect your own outcome!

The following is a list of statistics about financial security and the USA:

According to the US Census Bureau, the poverty rate in the United States was 9.2% in 2019, which equates to approximately 34 million people living below the poverty line.

The poverty rate is highest among children, with 14.4% of children under the age of 18 living in poverty in 2019.

Poverty rates are also higher among certain racial and ethnic groups. For example, the poverty rate for Black individuals was 18.8% in 2019, while the poverty rate for Hispanic individuals was 15.7%.

Financial insecurity is also a major issue in the United States. According to a survey by the Federal Reserve, 37% of adults in the United States would not be able to cover a $400 emergency expense without borrowing or selling something.

Additionally, a survey by CareerBuilder found that 78% of American workers live paycheck to paycheck, meaning that they would struggle to meet their expenses if their paycheck were delayed by even a week.

These statistics highlight the fact that poverty and financial insecurity are widespread issues in the United States, affecting millions of people. The financial system of the United States is not built for the people, and can be difficult to navigate effectively. The statistics also underscore the importance of personal finance education and support for individuals and families who are struggling to make ends meet. By understanding how to manage their finances effectively and take control of their financial situation, individuals can better navigate the challenges of poverty and financial insecurity.

Resources

US Census Bureau, “Income and Poverty in the United States: 2019”: This link corresponds to the first statistic, which is the poverty rate in the United States. It also corresponds to the second statistic, which is the poverty rate among children in the United States.

Maslow’s Hierarchy of Needs is a well-known psychological theory that outlines the fundamental needs that human beings strive to fulfill to achieve happiness and a sense of fulfillment. According to Abraham Maslow, individuals must fulfill their physiological needs, safety needs, love and belonging needs, esteem needs, and self-actualization needs in a hierarchical order to achieve self-actualization. While personal finance is not explicitly mentioned in Maslow’s theory, it is an essential aspect of fulfilling these needs, as it can either facilitate or impede the attainment of each level. You can learn more about Maslow’s Hierarchy of Needs here.

Physiological Needs

The first level of Maslow’s Hierarchy of Needs is physiological needs, which are basic necessities such as food, water, shelter, and clothing. These needs are essential for human survival, and they are the foundation upon which all other needs are built. Without these basic necessities, an individual cannot survive or function properly. Personal finance plays a crucial role in fulfilling these needs, as income is necessary to purchase food, pay for rent, and maintain a healthy lifestyle. A lack of financial resources can lead to malnutrition, homelessness, and other health issues, ultimately inhibiting an individual’s ability to fulfill their physiological needs.

The second level of Maslow’s Hierarchy of Needs is safety needs, which include a need for stability, security, and protection from harm. These needs are necessary for an individual’s physical and emotional well-being. Financial security is essential for fulfilling safety needs, as it allows individuals to invest in a stable home, healthcare, and insurance. Without financial security, individuals may struggle to meet their safety needs, leading to anxiety, fear, and a sense of instability.

Love and Belonging Needs

The third level of Maslow’s Hierarchy of Needs is love and belonging needs, which include a need for social interaction, intimacy, and a sense of connection to others. These needs are essential for human relationships and social support, which are critical for mental health and well-being. Personal finance can significantly affect an individual’s ability to fulfill their love and belonging needs. For example, a lack of financial resources can limit an individual’s ability to engage in social activities, pursue hobbies, and participate in events. Conversely, financial abundance can provide opportunities for travel, leisure activities, and other experiences that foster social connections.

Esteem Needs

The fourth level of Maslow’s Hierarchy of Needs is esteem needs, which include a need for self-esteem, respect, and recognition from others. These needs are necessary for an individual’s confidence and self-worth, which are critical for mental health and well-being. Personal finance can significantly affect an individual’s ability to fulfill their esteem needs. For example, financial resources can provide access to education, professional development, and other opportunities for personal growth. Additionally, financial resources can provide access to luxury items, travel, and other experiences that may increase an individual’s sense of self-worth and recognition from others.

The final level of Maslow’s Hierarchy of Needs is self-actualization needs, which include a need for personal growth, creativity, and the pursuit of meaningful goals. These needs are essential for an individual’s sense of purpose and fulfillment. Personal finance can play a critical role in fulfilling these needs, as financial resources can provide access to education, travel, and other experiences that allow individuals to pursue their passions and aspirations. Furthermore, financial security can provide individuals with the freedom to pursue careers or personal projects that align with their values and goals.

Personal Finance Can Help You Find Fulfillment

It is important to recognize that personal finance does not guarantee fulfillment of these needs, but rather enables individuals to have the necessary resources to fulfill them. For example, having financial resources does not guarantee fulfilling social connections, but it can provide the opportunity to engage in social activities that foster those connections. Therefore, individuals should be intentional about how they use their financial resources to fulfill their needs. Developing a personal finance plan that aligns with their values and goals is a critical step towards achieving a sense of fulfillment and happiness. My Financial Equity has free budget templates on our Resources page to help you get started on your path to fulfillment, because every financial plan includes a spending plan!

It is essential to prioritize spending in a way that satisfies the most critical needs first and then allocate resources towards less critical needs. This approach allows individuals to be more intentional with their spending and ensure that they are putting their resources towards activities that fulfill their needs. Additionally, budgeting and saving can provide individuals with financial security, reducing stress and anxiety and enabling them to pursue activities that align with their goals and values. Overall, personal finance plays a critical role in fulfilling Maslow’s Hierarchy of Needs, and individuals should be intentional about how they manage their financial resources to achieve a sense of fulfillment and happiness.

Credit plays a vital role in our lives and is critical to securing many of the things we desire and need. In this modern world, having good credit is incredibly important. It affects our ability to borrow money, secure a loan, and even get a job. Here are three reasons why you should start building your credit as soon as possible.

Better Loan and Credit Card Rates

Lenders often reward good credit scores with lower interest rates. Lower rates make it easier for you to borrow money for a home, car, or even a personal loan. When you have a high credit score, lenders consider you a low-risk borrower. Lenders can offer lower interest rates on loans and mortgages to low risk borrowers because they have proven the ability to pay back borrowed money. The higher your credit score, the better the interest rate you will receive. This can translate into significant savings over the life of the loan. However, you may have trouble getting approved for a loan if you have poor credit. If you do get approved for a loan, the interest rate will likely be high. High interest rates can make it difficult to repay a loan.

For example, a person with a credit score of 720 or higher is likely to receive a mortgage interest rate that is 0.25% lower compared to someone with a credit score of 680. Over the life of a loan, this can save you thousands of dollars.

Additionally, credit card companies also use your credit score to determine your interest rate. If you have good credit, you will likely receive a lower interest rate. That means you will pay less in interest charges and be able to pay off your debt faster.

Photo by Pixabay: https://www.pexels.com/photo/person-holding-debit-card-50987/

Access to Better Employment Opportunities

Employers are increasingly looking at credit scores when making hiring decisions. This is especially true for jobs that involve handling money or making financial decisions. Good credit is a sign of responsibility and reliability. Many employers believe that individuals with good credit are less likely to engage in financial misdeeds or embezzlement.

Having good credit can help open the door to better job opportunities. In today’s competitive job market, it’s essential to have a strong credit score to stand out from other applicants and increase your chances of landing your dream job.

Peace of Mind

Finally, having good credit can give you peace of mind. With good credit, you will have the financial stability to handle unexpected expenses or emergencies. This sense of financial security allows you to make big purchases, such as a home or car, without worry. Additionally, good credit can also help you in times of financial hardship, such as a job loss, medical emergency, or other unexpected expenses. With good credit, you have more options to access credit. That can include personal loans, credit cards, and lines of credit, to help you get through tough times. You also won’t have to worry about being unable to get a loan or being rejected for a job because of poor credit. You will be able to focus on your goals and live your life with confidence, knowing that your good credit score will help you reach your financial goals.

In Conclusion

Building and maintaining good credit is essential in today’s world. It can help you secure better loan and credit card rates, open doors to better job opportunities, and give you peace of mind. It’s never too early or too late to start building your credit. Start by getting a copy of your credit report, paying your bills on time, and keeping your credit card balances low. With a little bit of effort, you can have a strong credit score and enjoy the many benefits that come with it.

Struggling to stick to your financial goals? My Financial Goals Workbook can help—learn more here.

There are different ways that credit scores are calculated. Unfortunately, there is no agreed-upon method that all firms, credit unions, banks, etc., use to calculate credit. FICO and VantageScore are the most used models for credit scoring, but there are a few other scoring models. There are also a variety of scores made for specific purposes, such as purchasing a home or car. Learn ways to build credit in our article, 4 Ways to Build Credit Quickly.

FICO: One Way Credit Scores Are Calculated

The FICO score was created in 1989 to create a credit scoring model to make lending easier and unbiased. Classic FICO scores are calculated using payment history, credit utilization, credit history, types of credit, and new credit. This website goes more in-depth on FICO scores.

Requires More Attention

Payment history is 35% of the calculation. As long as you make payments on time and do not have any lawsuits, liens, bankruptcies, or foreclosures, you will score well in this part of the calculation. If your payments are late, it will affect your credit to the extent that it was late.

Credit utilization is 30% of your score. You should use a maximum of 30% of your credit limit, but it is best if you can keep utilization down to 10%. Using a maximum of 30% of your credit limit means that if you have a $1,000 limit, you should only spend $300.

Requires Less Attention

Credit history is 15% of your score. To make sure you score well in this category, you only need to make sure you make payments on time. This part of the score is something that you can only perfect over time.

Credit use is 10% of your score. This category is about the different types of credit you have. This can be credit cards, mortgages, auto loans, etc. This category is a little tricky because it wants you to have various types of credit, but you can’t apply for credit too fast, or it will be a red flag on your report. You can improve this category over time.

Last is new credit, which is 10% of your score. In this category, applying for a lot of new credit at one time will harm your score. It is best to apply for credit slowly. For example: You could get a secured credit card when you turn 18, and as you build credit, you should have the option to either change that card from secured to regular. Then maybe a couple years down the road, your credit might be enough to get a car loan. This adds to the variety of credit lines in your name and will increase your score (after the initial drop from the hard inquiry).

VantageScore: Another Way Credit Scores Are Calculated

The VantageScore was created in 2006 by the three credit bureaus (Experian, Equifax, and Transunion) to compete with the FICO credit score. This score uses payment history, age and type of credit, credit utilization, total balances, recent behavior, and available credit to calculate a score. These categories are weighted differently than in the FICO scoring model. NerdWallet goes more in depth on this scoring model here.

More Important to Focus On

Payment history has a high weight at 40%. With this category, you need to make payments on time. Any late payments will stay on your report for seven years, meaning they will continue to affect your credit for seven years. Fortunately, those late payments drop off your credit report after 7 years, which should raise your credit score.

The second category is age and type of credit. This category has medium-high weight at 21%. For this category, let’s say you have a good mix of credit with a 15-year-old mortgage, a 3-year-old car loan, and credit cards of varying ages, and you pay everything on time. You will do well in this credit category if you maintain a variety of different types of credit over a longer period of time.

Credit utilization also has a medium-high weight of 20% – similar to the last category. To calculate credit utilization, you divide your balances by your available credit. A rule of thumb for this category is to keep your utilization under 30%, but keeping it under 10% is even better. Having high utilization (more than 30%) will have a negative impact on your credit score.

Still Important, But They Have Less Impact

Total balances are the next category. It has a medium weight of 11%. This category counts your total debt, including current and delinquent accounts. For this category, lowering your total debt will increase your score.

Another category is “recent behavior”, which has a low weight of 5%. This category is about your new accounts and the number of hard inquiries you have. Keeping this number low will be better for your score. That means not opening new accounts very often – maybe once a year. Twice if absolutely necessary.

Lastly is available credit, which has an extremely low weight at 3%. This category is about the amount of credit you have available to use. Having more credit available to use can be good, as long as it fits with your reported income. Having too much available credit can impact your score negatively. The idea here is that having too much available credit makes a person riskier in the eyes of a lender. This person could attempt to use all of their credit and not be able to pay it back because they had too much available to them. This part of the scoring model has a low weight and cannot affect your credit score as much as the parts of this calculation.

Other Credit Scoring Models

There are other, less common credit scoring models. These include TransRisk, Experian’s National Equivalency Score, Credit Xpert Credit Score, CE Credit Score, and the Insurance Score. Then there are industry-specific credit scores. An example of this would be if you were looking for another credit card, the company would do a calculation based on your history with your other credit cards, and they may give you that credit card if you have a good history with credit cards.

Do you struggle to maintain your budget? That’s okay. A lot of people do. I’d like to help you learn how to budget better. Budgeting is an important part of managing money effectively. It helps you plan for the future and keep track of your spending habits. This guide will teach you how to start budgeting and how to keep budgeting, even when you don’t want to.

Know Where You Spend Money

Start by looking at where you spend your money. Are there any areas that you would like to cut back on? If so, what do you need to do to make those changes? Once you have identified these areas, start tracking your expenses. Make sure you are recording everything you spend money on. You can either start a budget and focus on tracking your expenses, or you can do this retroactively by looking over your bank statements for the last couple of months.

If you’d like to start a budget, I recommend looking at our Resources category for information on budget sheets. There are budget posts for a variety of difference pay schedules including weekly, biweekly, semi-monthly, and monthly. They each include a budget spreadsheet and explain how to use it.

Set Goals to Budget Better

It’s essential to set goals when you are trying to save money. You should set short-term and long-term goals because setting both types of goals can help you be more involved in your own financial success. An example of a short-term goal can include saving $100 per month or paying off an old debt. A long-term goal could be saving up for a $2,000 vacation or buying a new car with a down payment of $1,500. When you set goals, you are much more likely to achieve your desired outcome. You can learn more about goal-setting in this article.

Create an Action Plan

Once you have identified your goals, you need to develop an action plan to achieve them. This means creating a detailed schedule with dates and times for each task. If you have multiple tasks, break them down into smaller steps. Then, write out what you will do every day to accomplish those tasks. I recommend creating SMART goals. This stands for Specific, Measurable, Achievable, Relevant, and Time-bound.

SMART Goal Budget Example

Fran sets a goal to save money so she can move out. She decides that she wants to move out in two months, and the rent she can pay at her new apartment is $750. She will also need to come up with one month’s rent for the deposit, which means she will need to save a total of $1,500 before the two months are up. Fran can break this amount up between her paychecks, which she receives bi-weekly. $1,500 / 4 = $375 per paycheck for the next 4 paychecks.

Specific: She will save $375 per paycheck for the next four paychecks.

Measurable: She will save $1,500 in the time she needs it.

Achievable: Fran will save two months’ rent in two months.

Relevant: She needs to move into her own place.

Time-bound: Fran will complete this goal in two months.

Stick to it!

You should also make sure that you stick to your budget. It’s easy to spend more than you planned when you are excited about something new. However, if you find yourself spending more money than you expected, take some time to think about why you are doing so. Is there anything else you could cut back on? Are you using credit cards too much? Are you spending on things that you need, or things that can wait?

Regularly checking on and updating your budget can help keep you on track. I recommend budgeting for each paycheck, while also keeping the long-term in mind. The reason I like budgeting for every paycheck is that budgeting for every paycheck helps you see better what you are making, what you are spending, and when things are happening in your financial picture.

Don’t Be Afraid to Ask For Help

If you feel like you are struggling with your finances, talk to your friends and family members. They might not be able to help you directly, but they can give you advice and support. Getting support from your friends and family can increase your motivation to complete your goal and your chances of doing so.

I know it can be scary to ask for help or to let people know you are struggling, but my advice to you is to know the reason you are close to the people that you are close to. Would you expect them to judge you for any other reason? Have they helped you with other personal matters? If your answers to those questions are no, and yes, respectively, then I do believe that they would be more than happy to at least be someone you can lean on. Remember, you will get through this and you will learn how to manage your finances!

Struggling to stick to your financial goals? My Financial Goals Workbook can help—learn more here.

Budgeting is a lot easier to keep doing when you think positively about it rather than negatively. It is important to think of budgeting as something that can help you achieve your goals instead of something that only takes up your time. I use the phrase “spending plan” because it feels more positive to me than the word “budgeting.” I will use these words interchangeably in this blog because they are the same. If you find a word or phrase that helps you think positively about budgeting, use it. It can help keep you in a good budgeting mindset!

Three Qualities of a Budgeting Mindset

A good budgeting mindset is more of a set of qualities rather than one distinct way to think about budgeting. Those qualities are positive, realistic, and determined. While there may be other qualities that help you create the mindset for budgeting, these three qualities are essential.

Positive

Thinking positively about budgeting will help you keep doing it. One way to think about budgeting is that it is self-care. You are doing it to take care of yourself now and in the future. If you think of budgeting as a chore, or you cannot do it, or it’s too much, or it will not work, or that you do not make enough, then it will not be successful. If you go at it with optimism, you are much more likely to succeed. There is a solution to every problem; you just have to find it. Budgeting can help you get your money under control, learn more about your spending habits, pay off your debt, and plan for your financial future and these things can help you have a more fulfilling life.

Realistic

At the same time, though, you have to be realistic. Realistic about your spending habits, your income, and your debts. Being realistic about all of those things with yourself will help you create a better spending plan for yourself. If you are budgeting with a roommate or a partner, being realistic can be difficult. Being honest about money with the person you live with can create a financially happier household. Without it, you will likely struggle to keep up with or limit yourself in the categories you set for yourself. This can also emotionally strain a household if you or the person you are living with are having difficulties managing money.

Determined

You also have to be determined. If you are determined to create a budget, you will be much more likely to use it and therefore be much more successful. Having a reason to budget will help you be more determined to maintain your budget, even when you don’t want to. Your reason could be anything – paying off debts, growing your assets, finding financial freedom, or just getting to know your habits better.

Whatever you choose can change over time as your needs change. You paid off your debt? Fantastic! Maybe you can finally save up for that vacation you need. You can even have multiple goals for your money, but sometimes it is easier to only focus on one goal until you complete it and that is perfectly okay as well. Making SMART goals can help keep you focused and determined, and they are applicable to any part of your life! Learn more in this article from Forbes Advisor.

Budgeting Mindset: Conclusion

How you think about budgeting and your learning style can help you determine which form of budgeting is best for you. It might take some trial and error, but eventually, you will find the one that works for you. To find a way that works for you, you could think about your personality and learning preferences. Are you hands-on, or do you prefer to let someone or something else do it for you? Do you enjoy math? Are you a person who likes to plan? Do you prefer to use cash or a card? Paper and pen or spreadsheet? There are many questions you could ask yourself to learn what works for you.

Paper and pen will take the most work, spreadsheets are moderate, and apps take the work out of the equation. Each method requires planning, but an app might help if you need prompts. The envelope method is traditionally used for cash, so if you prefer cash or are hands-on, this may be a good method for you. You can learn more about this in the article, What Are the Types of Budgeting?

Struggling to stick to your financial goals? My Financial Goals Workbook can help—learn more here.

Budgeting is a financial plan for tracking, maintaining, and preparing your finances. Another term for budgeting is “spending plan”. The word budgeting can bring up negative thoughts of inflexibility and can feel like it is something tedious you have to do to get out of a mess. The term spending plan may feel more positive, and more proactive than the term budgeting. I will use these terms interchangeably. Budgeting can help you use your money in a way that benefits you, and there are several types of budgets, with some being hands-on and some that mostly do it for you.

Creating a spending plan can help you achieve realistic goals. It can help you keep out of debt, pay down debt, save for large purchases, save for retirement, etc. To create a spending plan, you need to start tracking your spending. If you use an app, it might do this step for you. Without this step, you might create a spending plan that does not reflect your actual spending. It is important to do this step to make the category limits accurate for your needs. When you have a realistic idea of your spending, you can create a spending plan that fits your needs and will allow you to make the necessary adjustments that you see fit. These adjustments are where you work to achieve your financial goals.

Budgeting Type 1: Spreadsheet

There are many ways to keep track of your money. One way to track your money is by using a spreadsheet. You can make one yourself, use one I have made available, or any number of the ones available on the internet. Spreadsheets are a hands-on method of a spending plan, which means you can organize it how you want. It can do the calculations for you if you plug in the right equations.

Using spreadsheets as your chosen method of creating a spending plan means you need access to a computer or smartphone. Another positive of spreadsheets is that you do not have to worry about putting identifying information such as your social security number or bank account information in them. Spreadsheets are versatile, so they can do just about anything if you learn how to use them. Spreadsheets are good for people who like to get really into budgeting and prefer to do everything themselves.

Budgeting Type 2: Envelope Method

Another type of budgeting is the envelope method. This method is also hands-on but does not require regular access to technology. In this method, you use envelopes or another kind of small bag capable of being labeled and holding cash. With this method, you can organize it however you want, and you also do not have to put any identifying information in them. The downside of this method is that you will have to do any calculations by hand. While traditionally, this method is physical, you can use this method in a spreadsheet, and some apps use this method as well. The envelope method is good for people who prefer cash over cards or are more visual.

Budgeting Type 3: Budget Tracking Apps

You can also use apps to track your spending. This type of budgeting is more of a set-and-leave-it kind of thing. They might have customizable categories, attach to your accounts, help you set goals and track where you are in those goals, and keep track of where you are spending. There are more than a dozen different personal finance apps to choose from. Apps have varying degrees of being hands-on as well as varying degrees of success in linking to accounts and successfully applying expenses to the proper categories. Apps are a good choice for those who do not have the time or would prefer not to take the time that other methods might require. You can check out this list of budgeting apps from Forbes Advisor, to learn more about specific budgeting apps.

Struggling to stick to your financial goals? My Financial Goals Workbook can help—learn more here.

I will go over everything you need to know about using this spreadsheet template including where to put your income and expenses, how to use the income estimation box on the side, how to make new sheets within the spreadsheet, and how to copy the spreadsheet for a new year. You can download your free weekly budget template here. If you would like to check out our other budget templates, you can see them on our Resources page.

I like to use google sheets for my budget templates because they are free, customizable, and don’t require any of my personal information. You can also convert google sheets into excel spreadsheets if you prefer to use excel. The great thing about this conversion is that you can do it without any loss to the formatting or calculations.

Where to put your income

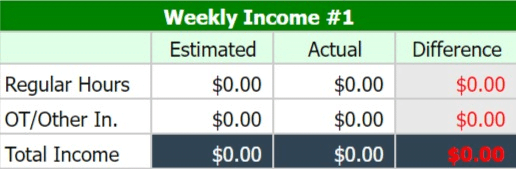

There are four boxes for income on each month’s sheet, for each of the four weeks in a month. The image below shows what those boxes look like.

The first column shows the type of income it is, the second column is for the estimated amount you will receive, and the third column is for the actual amount you receive. The fourth column shows the difference between your estimated and actual amounts by subtracting your actual income from your estimated income. You can either use your current paycheck for the estimated column or you can use the income estimation box on the far right of the google sheet. The estimated income column is preset to use the income estimation box outcomes.

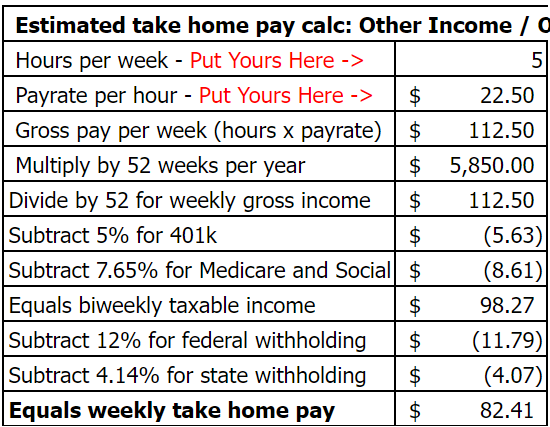

How to use the income estimation boxes

The income estimation boxes use your weekly hours and hourly rate to calculate your after-tax paycheck. It also includes a row for your 401k or other pre-tax retirement contribution that comes from your paycheck automatically. This row is preset for a 5% contribution amount but it can be adjusted to whatever percentage you personally contribute – or it can be changed to 0% if you do not participate in any pre-tax retirement plan.

This is what the income estimation box looks like for your regular hours. You start with your weekly hours and then enter your hourly pay. From there, it automatically calculates your weekly income, which shows at the bottom of the box. You can change the amount for your 401k by entering a new decimal amount in place of the current decimal. At the current preset of 5%, the equation looks like =-V11*0.05. To make it 3%, you would only change the 0.05 to 0.03.

There is another income estimation box underneath the first one. This one can be used to calculate the amount you will make in overtime or if you have a second job. All of the customization rules for the first box also apply to the second box.

If you are using it for a second job, you will use it exactly like the first income estimation box. If you are using it to calculate how much you might make in overtime, you will type in the following equation: = Regular pay rate + (Regular pay rate/2). An example of this would be =15+(15/2). The cell will calculate this number for you, and then it will finish the calculation for the income estimation.

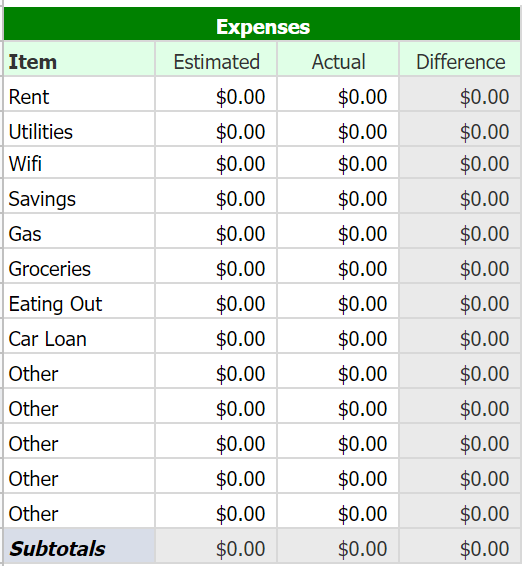

Where to put your expenses

Under the income section of the free weekly budget template, there is a row that adds up your monthly income and shows the difference between what you expected to get for the month and what you actually made. Then below that is the expenses section. There will be four of these expense boxes – one for each week. They look like the box to the right of this text. Each of those categories are completely customizable to your needs, and I recommend budgeting for bills for the week of your paycheck. An example of this is if you have a bill on Monday and you get paid on Friday, then you would budget for that bill on the Friday before that Monday.

Just like with the income section, the expense section will show the difference between your estimated and actual expenses. As you get familiar with your expenses, you should be able to adjust your estimated amounts to be closer to your actual spending.

Underneath the expenses section, are two more sections. Directly underneath this section will be the expenses total summary section. This section shows your estimated expenses, actual expenses, and the difference between the two for the entire month. The last section is the monthly balance summary. This section shows your cash flow for the month – all of your expenses, all of your income, and then it will show you whether you spent more or less than you made for the month.

Google sheets tips

How to create more sheets within an existing spreadsheet.

If you need to make more sheets within the existing sheet, you start by right-clicking on one of the months at the bottom. This will show some options, and the one you need to click on is “Duplicate”. Then you can click and hold onto that sheet to move it to where you need it. Doing this will copy an existing sheet but keep it in the same document.

How to make an entirely new sheet for the new year.

If you need to make a new spreadsheet, you will start by clicking on “File” at the top left of the page. Then you will click “Make a copy”, which you will see in the first section of the drop-down menu. After that, you will see a pop-up with an option to rename the new sheet you are creating, as well as move it to a new place in your drive – if you so desire. You can also come back here for next year’s free weekly budget template!

There are several ways to budget, and it’s just a matter of finding the way that works for you. One way to do that is by your learning style – if you know which style is yours. Another way is deciding whether you want to be hands-on with your budget or not. The third way to find out is by deciding if you want to spend money on an app or do it yourself. Last but not least, I will explain the pros and cons of automating transactions.

Learning styles

There are four learning styles – visual, auditory, reading/writing, and kinesthetic. Patterns and shapes may work best for you if you are a visual learner. These can include graphs/diagrams, which you can find in apps or create in a spreadsheet.

Speaking your thoughts helps you articulate them if you are an auditory learner. This means that it does not matter if you use an app or make a spreadsheet because you would need to explain it out loud either way.

If you learn best using reading/writing, you understand information when it is in written form. Same as auditory learning, it does not matter which you use because either way, your budget will be in written form.

If you are a kinesthetic learner, you learn through doing. With budgeting, you can use personal experiences. Take what you have done in the past and learn from that. If you have not budgeted before, you can use trial and error. It would help to get to know your spending and tweak it as needed.

Hands-on or not?

Are you a hands-on person? You may prefer spreadsheets, notes, or the envelope method if you are. Spreadsheets can help you do the math, and you’ll be able to make charts or diagrams if you like. When I say notes, I mean just jotting it down on a piece of paper or in your notes app. Then with the envelope method, you can use actual envelopes or an app/spreadsheet that mimics the envelope method.

If you are a hands-off person, you might prefer forms of budgeting that require less control. If you have a steady income, budgeting like this could look like setting a budget and then creating auto transfers within your accounts. Some apps help you do this as well.

Spend on an App or do it Yourself?

One thing you have to consider when deciding to spend money on a budgeting app is the cost of doing so. There is almost always a free version of an app, and it is best to try that version first. That version is more than enough for your needs most of the time. If it is not, you could consider trying other free apps, but if you are dead set on one app, then spending the money on it might be worth it. Investopedia has a list of budgeting apps that they recommend here.

The risk involved in using a budgeting app is also something to consider. Apps connect directly to your accounts to pull data from so you can use the app. This means that your accounts could be hacked because you have to allow that app constant access to them. Your bank could be hacked even if you do not use an app, but the more your information is out there, the higher the chance that something might happen.

The reward associated with using an app is also important to think about when deciding to use one for budgeting. Using an app could take less time than budgeting by hand or using spreadsheets. Apps may also have reminders or notifications that you might find helpful. These things might allow you to focus more on the things you want to focus on instead of spending time doing something you do not want to do.

Pros and Cons of Automating Transactions

The Pros:

1) It can make things easier if you do not want to transfer money around your accounts every time you get paid. Your bank will transfer the money for you at the time you scheduled for it to do so.

2) It can make things easier if you have a money disorder. This can include gambling or impulse spending. Automating transfers can help you keep your money safe in case something happens.

The Cons:

1) It can make things difficult if you need full liquidity. People who need full liquidity are usually people who live paycheck to paycheck. A lot of the time, automating transactions can make your money less liquid, and when you live paycheck to paycheck, you need as much liquidity as possible in case something happens.

2) Forgetting about automated transactions can cause you to overdraw your account. If you automate and do not have a consistent paycheck or forget the schedule you set when you automate transactions, you could overdraw your account.

Struggling to stick to your financial goals? My Financial Goals Workbook can help—learn more here.